The world’s wars – Ukraine started using long-range weaponry from the U.S and U.K to hit targets inside Russia. Russia, of course, retaliated by launching a large overnight missile barrage at the Ukrainian power system, with Putin threatening to strike decision-making centres in Kyiv with new ballistic missiles. Trump named a former general, Keith Kellog, as special envoy to Ukraine-Russia, with plans for a peace deal and which likely will allow Russia to keep Ukrainian land.

Meanwhile, the current U.S administration brokered a ceasefire between Israel and Hezbollah in Lebanon – suspending nearly a year of hostilities – bringing hope to a possible peace deal in the region.

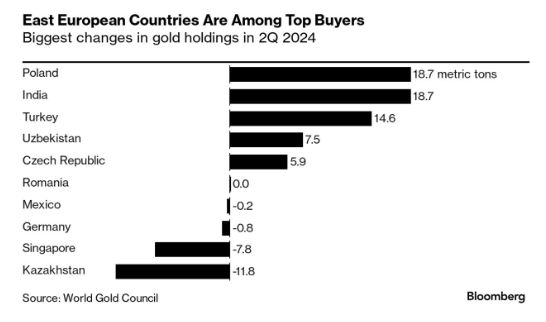

Easter Europe is rising – quietly growing and stocking up on gold. Uzbekistan has experienced robust economic growth in recent years. In 2023, its GDP grew by 5.99%, up from 5.67% in 2022. This upward trend continued into the first quarter of 2024, with a year-over-year growth rate of 6.2%. Growth in the Visegrád countries - Poland, Czechia, Slovakia, and Hungary - are expected to reach 2.5% this year. They’re now further strengthening their balance sheets with gold.

Debt Sales and Stimulus Galore – Europe has opted to borrow a new record amount of money by issuing $1.8 trillion of bonds this year, passing the high-water mark previously set in 2020. They’re on a borrowing spree to finance ever-growing debt piles amidst pedestrian growth in the region, and the real risk of recession.

China is embarking on a monster stimulus package over the holiday period, the biggest in Chinese history, and which imitates the more recent money printing packages of 2008-2009 American QE’s and Japan’s current one. After growth slumped in the last 5 years to the 4 to 6% mark, versus the 8 to 10% GDP figures in the three decades before that, the communist government is aiming to reinflate Chinese property and stock market prices, whilst assisting local governments with their CNY 65 trillion debt problems.

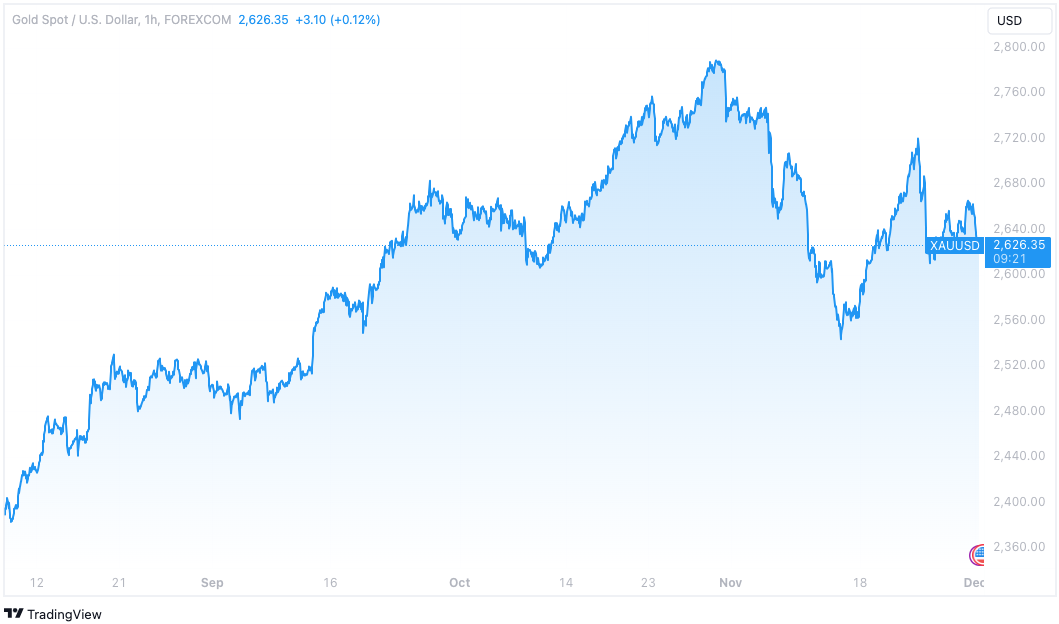

Gold has come off its record highs ($2,800/oz) post the U.S election, with gold declining 3% in November. Election results gave more certainty on the economic and policy direction of the world’s largest economy, boosting the Dollar into a short rally, with the greenback gaining 2% in the same November month.

Gold is currently seen trading at above $2,626/oz – above support at about $2,570 but not yet testing the resistance levels of $2,675 - $2,685/oz. For South Africans, the Rand gold price shows strength above R47,000/oz, trading at R47,690/oz – slightly off its November high of R49,180 and its all-time high of R49,300 in October.

However, the structural drivers of the gold price remain sound. According to Goldman Sachs, gold is set to rally to a record $3,000/oz next year on central bank buying and US interest rate cuts. In a recent note, the bank’s analysts said, ‘Go for gold.’ The bank reiterated that although Trump’s win strengthened the Dollar in the short term, his trade policies favouring levying tariffs, the fiscal unsustainability of the government’s finances, and other central banks’ sustained bullion buying to diversify away from US Treasuries, would fuel gold’s rally upward to $3,000/oz.

From a fundamental perspective, what’s driven the gold price down was market expectations around interest rates. As I’ve elucidated in previous notes, the main economic driver for gold price movements should theoretically be real interest rates i.e Dollar interest rates minus U.S inflation. If these real rats are expected to increase, then the opportunity cost of holding gold, and foregoing interest on Dollar deposits, rises – and vice versa.

This is exactly what’s been happening: markets anticipate Trump’s trade policies and proposed tax cuts will be inflationary by fuelling larger budget deficits that the government has to finance through inflation. In order to stem inflation, the Fed would likely need to maintain higher real rates in the economy, and hence put pressure on gold.

However, famed investor Jim Rogers said on a podcast this past week, that even though inflation isn’t finished, the US is enjoying the longest period of ‘good times’ in the nation’s history, and that markets are in a bubble – ‘everybody’s just been winning.’ This longest period in U.S history without a recession is due to massive amounts of money printing, he says, and the U.S economy isn’t healthy, and is saddled with immense debts. Consequently, we could see a bubble burst, which would force the U.S Fed to try to reinflate the bubble and restimulate asset prices, because it is politically expedient.

This will drive gold prices higher, as gold has become a barometer for the fiscal and monetary policy actions undertaken by global governments. Gold remains on the launchpad.