Iran Attacks Gulf Energy –

The U.S and Israel commenced attacks on Iran’s leadership, nuclear and military infrastructure on 28 February 2026. The Iranian regime retaliated with drone and missile attacks on U.S footprints in the Gulf region – the U.A.E, Oman, Iraq, Syria etc. In addition, Tehran has overseen a near complete closure of a key global economic oil choke point, the Strait of Hormuz – an attempt to shock and destabilise the global economy, thus applying pressure on the U.S to deescalate the conflict.

The assault on global fuel supply has worked, with the price of crude having risen 60% since the war started. Wall Street closely monitors the price of crude, particularly a grade called West Texas Intermediate (WTI) that trades in New York and a second called Brent traded in London. It’s a benchmark followed by everyone, from bond investors to central bankers. But only oil refiners buy crude — and are therefore exposed to its price. The real-world purchases refined petroleum products such as gasoline, diesel and fuel oil, so it’s those post-refinery prices that matter to consumers.

US vs China –

Trump also said he had requested China — among those he’s asked for support — to delay a summit with Xi Jinping for about a month, saying it was important for him to remain in Washington to oversee the war. With what would likely be a historic showdown when the two presidents meet, pundits have suggested that the U.S started the Iran conflict, in an attempt to gain a key leverage point in the upcoming negotiations. With America having seized the Venezuelan oilfields, they could hold a decisive bargaining chip against China if they controlled Iranian oil – Venezuela and Iran are major suppliers of oil to China.

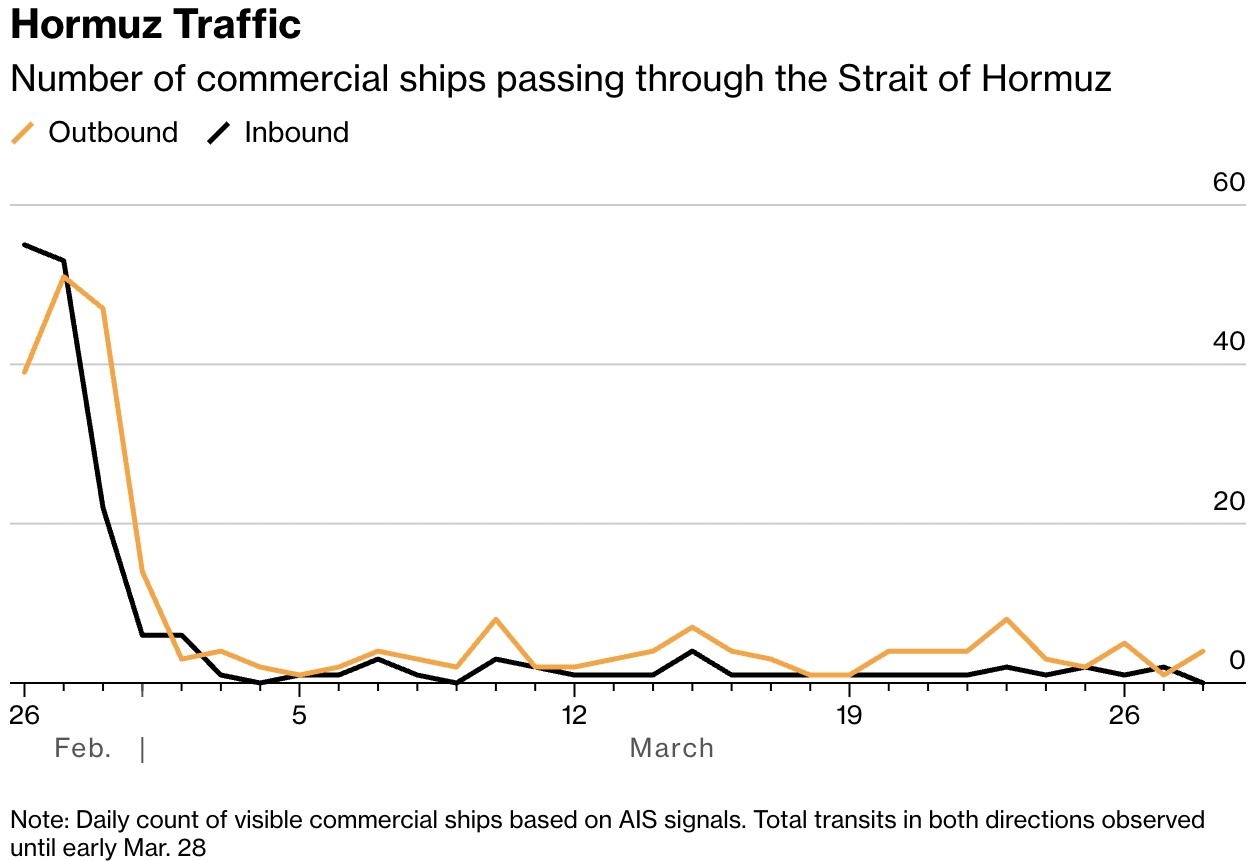

Oil Supply Shock -

Trump also renewed calls for allies to help safeguard and re-open the Strait of Hormuz. Shipping through the waterway has ground to a near-halt – a normal rate of 20 to 21 million barrels a day has collapsed to between 0 and 0.5 mbpd. These 20 million barrels account for 20% of the world’s daily oil.

U.S President Trump has offered Iran a peace deal, which essentially offered Tehran sanctions relief in return for it dismantling nuclear facilities and reducing its missile arsenal, as well as reopening Hormuz. Iran, for its part, is insisting on war reparations, recognition of some form of control over Hormuz and pledges that the US and Israel won’t attack it in the future. Iran has rejected the 15-point plan.

“The biggest risk in the market is the Strait of Hormuz remaining constrained for a longer stretch and the market feeling the US and its allies have a limited capacity to alter the dynamic,” said Chris Weston, the head of research at Pepperstone Group in Melbourne for Bloomberg, March 17.

Source: Vessel tracking data compiled by Bloomberg – 2 April 2026.

Impact on Inflation– Surging oil prices triggered by the Middle East (Hormuz) conflict is likely to push global inflation higher and see policymakers keep interest rates unchanged for months, according to Morgan Stanley. Higher oil prices raise fuel costs directly, and the geopolitical uncertainty drives inflation expectations – this weakens currencies like the Rand that is used to import oil to SA and should keep interest rates at elevated levels.

“The implication is a materially longer hold (interest rates) rather than an immediate tightening response,” Morgan Stanley economist Andrea Masia wrote in a research note. Morgan Stanley sees South African inflation accelerating temporarily and growth taking a hit this year.

Gold reached a new record high of $5,593/oz at the end of January. Since then, on the back of the Iranian conflict, the price moved strongly lower to a level of $4,200/oz, before recovering to the $4,600 level today.

In our previous note, we provided a pundit’s view on forward-looking gold prices. Standard Bank’s Adrian Hammond, the bank’s head of precious metals, said that gold is likely to soar above $7,000 an ounce, and possibly even breach $10,000. “We have a high conviction that gold will end above $6,000 this year. For next year, our base case is $7,000 depending on your view of interest rate cuts, but we think three cuts will get you there, and any further cuts will get gold between $8,000 and $10,000.”

With oil prices above $100 a barrel, the inflationary shocks globally will keep interest rates likely flat to higher – as central banks turn hawkish in their attempt to curb this inflationary impact. This, primarily, is why we’ve seen gold prices take a hit. One has to consider then whether this affects the fundamentals driving gold’s recent surge, or whether this is a temporary bump in the road.

Gold prices took off because of structural monetary shifts in the global financial, trade and political system. Specifically, massive government debt levels accompanied by deficit spending and budget deficits accelerating, meant that currencies were being debased, and particularly the view that the Dollar would lose its hegemony (the Debasement Trade). This led to a structural dedollarisation by big holders and buyers of gold i.e. central banks, as they started shifting away from holding Dollars and Treasury Bonds as reserves in the same allocations and quantum’s as before.

However, central banks buying gold to cushion their economies from macro risks continues – the World Gold Council released February data, stating, “February seems to indicate a rebound in central bank buying after a quiet January, highlighting commitment to gold’s role in reserves. At the same time, central banks may be prudently price sensitive in their accumulation. Poland's contribution this month highlights continued appetite from established buyers, with persistent buying streaks from Czech Republic, China and Uzbekistan signalling sustained demand.”

In the shorter term, the current decline in gold is a result of a rare alignment of economic forces. While geopolitical tension usually supports the metal, the combination of a recently dominant dollar, higher bond yields (gold competes against yielding U.S Bonds), and urgent liquidity for traders’ needs, has overwhelmed the safe-haven narrative. The market is prioritizing cash and yield at the moment – but the fundamentals driving gold up, especially the inflation that will filter through goods and services prices as a result of Iran, is set to continue.

The yellow metal was last seen trading at $4,626/oz.

Source: TradingView – XAUUSD (1 month), 2 April 2026.